The tax system treats the majority as the exception

- Nite Tanzarn

- May 1

- 5 min read

Tax systems do not reflect economic life. They structure it around assumptions about income, time, and visibility.

They are built on an implicit model of the taxpayer — stable income, formal employment, individual responsibility, linear time.

This model is not descriptive of the economy. It is a design choice.

And it is a narrow one.

The result is not that some people fall outside the system. The result is that the system defines the majority through categories that do not fully recognise them.

Women, informal workers, and hybrid livelihoods are not outside the tax system.

They are inside it — but misclassified by it.

What is normal in the economy is treated as deviation in tax administration.

Who does the tax system recognise as its centre — and who is continuously repositioned as its exception?

Informality is not outside the system

Tax systems are often designed as if there is a clear boundary between formal and informal activity.

On one side: registered businesses, salaried employment, documented income.

On the other: everything else.

But the lived economy does not follow this separation.

Income is layered. Work is fragmented. Livelihoods move between trading, caregiving, farming, casual labour, and small enterprise. These are not exceptions. They are common economic realities.

Yet the system continues to treat them as outside its core logic.

Informality is not a gap in the system. It is what the system fails to fully recognise.

What happens when the majority economy is treated as outside the system designed to govern it?

Misclassification of the majority

Tax administration depends on classification: formal/informal, employee/self-employed, registered/unregistered, compliant/non-compliant.

These categories assume stability. The lived economy does not offer it.

A woman may run a small shop, support household farming, take on seasonal work, and manage care responsibilities. These are not separate identities in practice, but the system forces them into a single administrative category.

A market trader is registered as a “small business,” regardless of whether her income comes from multiple informal streams. A caregiver who earns intermittently is treated as economically inactive in periods where she is not visible in formal records.

Complex lives are compressed into simplified categories.

What does not fit the category is not adjusted for. It is absorbed, distorted, or ignored.

The system does not simply record reality. It restructures it into administratively manageable forms.

Who is flattened to fit the system — and who is recognised in full?

The category becomes the problem

When lived reality does not match administrative categories, the mismatch is rarely treated as a design issue.

It is treated as a compliance issue.

Irregular income is treated as instability — not because it is unstable, but because the system is built around regular income.

If work is informal, it is treated as non-compliance.

If records are incomplete, it is treated as failure.

But these are not deviations from economic reality. They are deviations from the model.

The problem is not people’s economic lives. The problem is the categories that cannot hold them.

If you do not fit the category, you become the category’s problem.

What happens when the system does not adapt to the reality it governs?

Visibility determines recognition

What is visible to the system becomes real to the system.

Formal employment generates records. Salaries leave digital traces. Registered businesses produce documentation.

Informal work does not always appear in these forms. It is cash-based, mobile, seasonal, or embedded in household economies. It is economically real, but only partially visible to the system.

What cannot be consistently recorded becomes inconsistently governed.

This is not absence. It is structured invisibility.

And invisibility is not passive. It shapes how people are classified, assessed, and treated.

In tax systems, what is not seen is not only excluded — it is reinterpreted.

What happens when visibility becomes the condition for recognition?

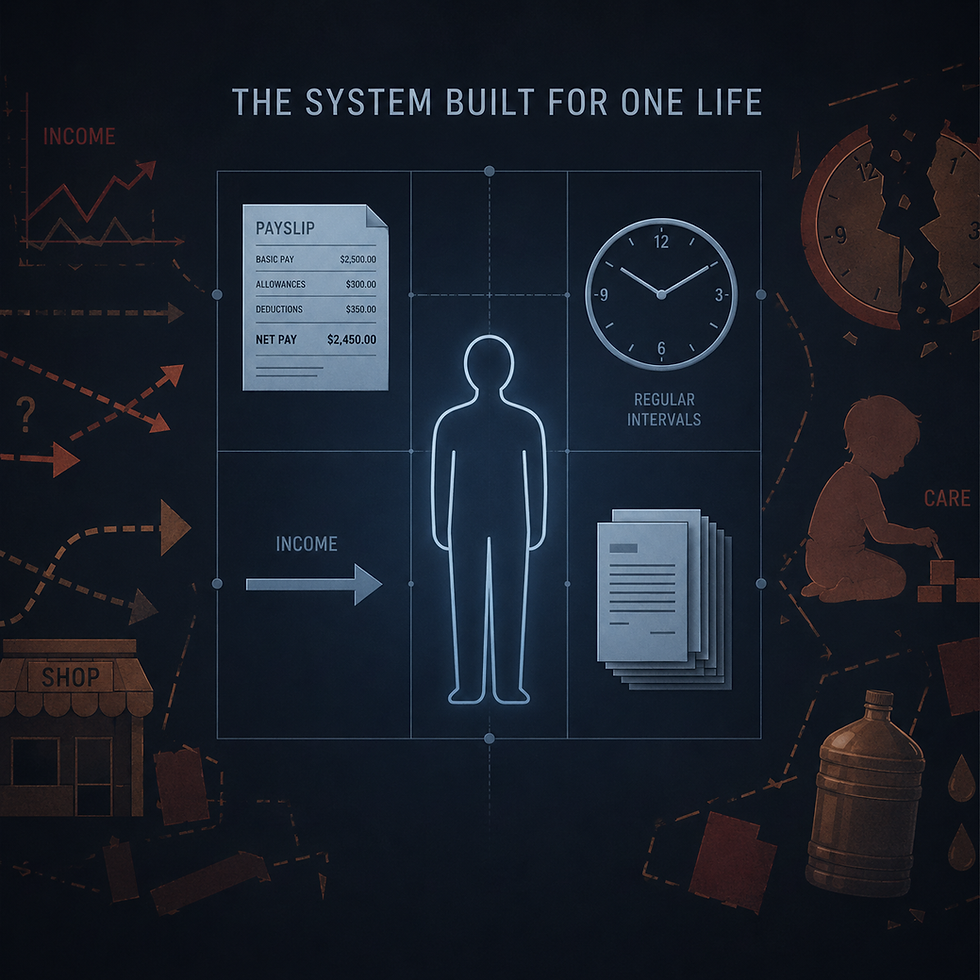

Design produces the “exception”

Tax systems do not reflect economic life. They structure it around assumptions about income, time, and visibility.

Stable income. Predictable employment. Individual taxpayers. Linear time.

These assumptions shape registration systems, filing requirements, payment structures, and compliance expectations.

But these assumptions do not reflect how most people experience work.

When design is built around a narrow model, everything outside that model becomes deviation.

This is not a mismatch in implementation. It is a design outcome.

The system does not exclude the majority explicitly. Exclusion is produced through a model they do not fully match.

That is enough to turn the majority into exceptions.

These assumptions extend beyond design.

They are embedded in rules, data systems, compliance requirements, and enforcement practices.

They are continuously reproduced.

Who was the system designed to fit — and who was designed out?

Governance through misalignment

When classification, visibility, and design do not reflect lived reality, governance becomes misaligned from the start.

The system governs as if the norm is stability, legibility, and predictability — and treats anything outside that model as deviation.

It governs as if formal employment is the baseline, while informal and hybrid livelihoods are treated as edge cases.

It governs as if the majority must adapt to the system, rather than the system adapting to the majority.

This reflects a system designed around a minority prototype presented as universal.

The majority are not outside the system. They are inside it — but treated as if they do not belong to its core logic.

This is how misclassification becomes governance.

The consequence

The tax system does not exclude the majority.

It includes them through categories that do not reflect their reality.

That inclusion is conditional, partial, and often distorted.

This misfit is not abstract. It is lived.

It appears as time lost to compliance, income lost to interruption, care stretched to accommodate systems that do not account for it. It appears as reproductive and maternal burdens carried alongside administrative demands. It appears as economic activity that is real, but not fully recognised — present in practice, absent in design.

Tax is paid in money. It is also paid in time, care, and economic possibility.

Women and informal workers are not exceptions to the system. They are central to the economy the system claims to govern.

But when they are treated as exceptions, the system misreads its own centre.

And when the centre is misread, the rules that follow are structurally misaligned from the beginning.

What happens when the majority is governed as if they are an exception to the reality they already represent?

What happens when the majority is required to fit a model they never shaped?

What happens when the system continues to enforce that model through its rules, data, and compliance structures?

What happens when this misfit becomes a site of extraction — of time, income, care, and economic possibility?

What happens when this becomes ordinary — not as failure, but as the system’s logic?

Closing insight

The system is not built around the majority it governs.

It is built around a prototype: stable, continuously employed, formally recognised, and unburdened by care.

That prototype maps onto a specific economic life — typically male, formal-sector, and institutionally visible.

For those who fit, the system works.

For the majority, it extracts — time, income, care, and economic possibility.

And because this extraction is normalised, it no longer appears as injustice. It appears as participation.

This is how the majority becomes the exception — and how tax injustice becomes ordinary.

Tax injustice is not only what is taken in money. It is what is taken in time, care, and possibility — from those the system was never designed to fit.

Next: The Tax No One Names

What do women pay that no one records? Unpaid care work as a hidden, non-monetary tax.

Comments