Intersectionality and tax justice – Which women?

- Nite Tanzarn

- Mar 25

- 7 min read

This series is for those who read “Do You Pay Your Taxes?” and wanted more. The voices in that article asked honest questions. Where does our money go? Why does the system feel rigged? Why do women bear the heaviest burden?

This series provides the answers, one layer at a time. Each piece examines a different dimension of tax justice through a feminist political economy lens. Together, they reveal the architecture of a system designed by the powerful, for the powerful. And they show what it takes to change it.

Some examples reappear across pieces. This is deliberate. Certain mechanisms—presumptive tax, the taxation of necessities, the unpaid care economy, the invisibility of informal workers—are so foundational that they deserve to be seen from multiple angles. Each time we return to them, we see another layer of how they operate.

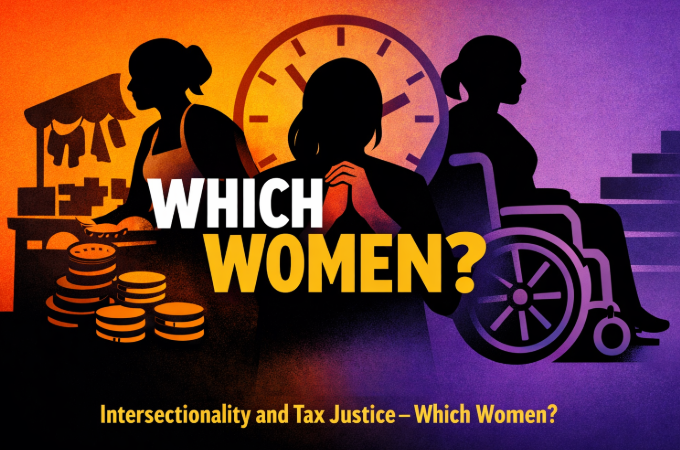

This series focuses on women. Not because they are the only ones made invisible by the system, but because their exclusion exposes tax injustice most clearly. Men are also excluded, also unseen. And women are not a single story. The market trader, the rural farmer, the woman with a disability—each faces different barriers. This article examines those differences directly.

Not “women”. Which women?

When we say tax affects women, we must ask: which women?

A rural woman farming on family land faces different challenges than an urban professional with a formal salary.

A young woman seeking her first job faces different barriers than an older woman caring for grandchildren.

A woman with a disability faces different obstacles than one without.

A refugee woman, an internally displaced woman, a woman in a conflict zone—each navigates a different tax reality.

Intersectionality insists we see these differences.

It rejects the assumption that a single policy affects all women the same way.

It demands responses that reach the most marginalised, not just the most visible.

Tax is not neutral.

And neither is gender.

Tax is experienced differently because life is lived differently.

Intersectionality is where that difference becomes visible.

The woman in informal trade: taxed daily

Market vendor. Street trader. Small‑scale cross‑border trader.

She is taxed early. Taxed daily. Taxed at the point of entry.

Market fees. Local levies. Transport deductions embedded in movement.

Not one tax. Many micro‑taxes stacked into survival.

She does not see the state once a year.

She meets it every day.

The woman in precarious formal work: taxed on scarcity

Cleaner. Domestic worker. Security guard. Retail assistant.

In many developing economies, domestic workers and retail assistants are not formally employed—no statutory contributions, no pension. Their work is formal in appearance, precarious in reality.

She enters the tax system through wages. PAYE. Payroll deductions. Statutory contributions.

But her wages are already compressed.

So taxation is not only deduction.

It is reduction on already reduced income.

She is taxed on scarcity. Not surplus.

The woman in subsistence and rural economies: taxed through cost

Farmer. Caregiver. Household manager.

Her economy is partially monetised, partially invisible, always stretched.

She may not be directly taxed in formal terms.

But she is heavily affected by indirect taxation.

Fuel. Transport. Goods. Inputs. Food.

Every increase moves through her household first.

She absorbs the system through cost, not through payroll.

The woman in unpaid care economies: taxed in time

She is not “outside” the economy.

She is holding it together.

Childcare. Elder care. Illness care. Household labour. Community care.

Unpaid. Unrecorded. Unrecognised.

But it has a tax. A time tax.

Because time is not free. And hers is already allocated.

Every hour spent on care is an hour not spent earning income.

That is not absence. It is economic extraction through expectation.

The cost of being female: reproductive tax

All women, across categories, encounter taxes tied to biology.

Sanitary products. Menstrual health costs. Reproductive healthcare.

Antenatal care. Delivery costs. Postnatal recovery costs.

Breastfeeding support. Milk formula when needed.

These are not optional goods. They are recurring obligations of the body.

Yet they are priced as commodities, not as necessities.

So the body becomes a site of continuous taxation.

Before income. Beyond income. Alongside income.

This is the reproductive tax.

It is rooted in biology.

It will not change with technology.

It should not be taxed.

The cost of care: care tax and time tax

Separate from biology are the socially ascribed roles of care.

Cooking. Cleaning. Washing. Fetching water. Collecting firewood.

Caring for children, the sick, the elderly, the disabled.

These are not biological imperatives.

They are roles assigned to women by society.

They generate two overlapping taxes.

Care tax: The direct costs of fulfilling these roles.

Taxes on cooking fuel, cleaning products, children’s food, medicines.

Every necessity for care is taxed, and the burden falls on the woman who provides it.

Time tax: The hours stolen from women’s lives.

Time spent on unpaid care is time not spent earning, resting, or participating.

It is extracted without record, without compensation, without recognition.

No receipt. No ledger. No exemption.

Just accumulation.

Indirect taxes: the burden none escape

Then there are taxes that touch all women.

Across class. Across sector. Across location.

Value‑added tax. Fuel taxes. Transport costs. Food price inflation. Commodity taxation.

These are indirect taxes. But their impact is direct.

Because women spend a larger share of income on essentials.

Because women manage household consumption.

Because women absorb price shocks first.

Indirect taxes are not neutral.

They are distributed through survival.

The rural woman: taxed, unseen

Consider the rural woman in eastern Uganda.

She grows maize on a small plot. No bank account. No identification documents. No formal income.

She sells at the local market, cash in hand.

The tax system does not see her directly.

But she pays VAT on everything she buys—salt, sugar, soap, paraffin.

She contributes to revenue. She receives nothing in return.

The nearest government clinic is fifteen kilometres away.

The road is impassable in rain.

The school her children attend has no desks, no textbooks, no paid teachers.

The taxes she pays flow to Kampala.

They do not flow back.

The woman with a disability: taxed without accommodation

Consider the woman with a disability in Kampala.

She runs a small stall selling vegetables.

She faces discrimination in access to finance, to markets, to information.

She incurs additional costs for transportation, for assistance, for healthcare.

The tax system offers no deductions for disability‑related expenses.

It assumes she is the same as the able‑bodied woman selling vegetables next to her.

She is not.

In Uganda, the law offers her some tax relief:

Exemptions on assistive devices, employment incentives.

But to access them, she must register with the National Council for Persons with Disabilities.

Obtain a Certificate of Disability.

Apply through the Council.

Wait for the Uganda Revenue Authority to issue a Tax Exemption Certificate.

Valid for three years.

Subject to review.

Each step assumes mobility, literacy, time, advocacy.

Each step assumes she knows the process exists.

How many women with disabilities can navigate this?

How many can afford to import the devices that are tax‑exempt?

How many ever see the relief the law promises?

The exemption exists on paper.

She lives on the floor.

Because tax‑funded infrastructure fails her daily.

A maternity facility has a bed—but she cannot climb onto it.

She delivers on the floor.

A toilet is separate—but she crawls on a floor that has not been cleaned because workers have not been paid.

A public service vehicle exists—but she cannot board it.

She pays taxes.

VAT on everything.

Market fees.

Transport levies.

She receives nothing that accommodates her.

Double taxation.

Being a woman.

Being a woman with a disability.

The system taxes her.

It does not see her.

It does not build for her.

And when she cannot use what her taxes built,

she pays again—in dignity, in safety, in time, in health.

The young graduate: taxed in survival

Consider the young woman graduating from Makerere University.

She has a degree but no job.

She enters the informal economy, selling cosmetics door to door.

She pays no direct tax because she has no formal income.

But she pays VAT on everything she buys to resell.

Her potential is untaxed. Her survival is taxed.

The system that educated her now extracts from her poverty.

The displaced woman: taxed outside the contract

Consider the older woman in a displacement camp in northern Uganda.

She fled conflict years ago. No land, no property, no formal rights.

She depends on humanitarian assistance and small trading.

She pays taxes she does not know she pays—VAT embedded in the price of every good she buys.

She receives nothing from the state because the state barely acknowledges her existence.

She is outside the social contract entirely.

The repetition of inequality

She pays at the market. She pays at the clinic. She pays in transport.

She pays in time. She pays in care.

Different points. Same burden.

Not repetition of error.

Repetition of design.

What tax justice must see

Tax justice cannot begin with systems alone.

It must begin with positioning.

Who is being taxed?

How are they located in the economy?

What do they already carry before taxation even begins?

Because neutrality does not exist in lived experience.

Only distribution does.

And distribution is always political.

Built into the body. Built into the day.

For many women, taxation is not a once‑a‑year event.

It is daily. Physical. Material. Temporal.

It enters through markets. Through movement. Through care. Through the body itself.

And yet it is rarely named in full.

This is the point

Tax is not only about revenue.

It is about structure.

And structure decides who carries what.

So when we ask about tax justice,

we are also asking:

Who is overburdened without recognition?

Who is contributing without visibility?

Who is paying in ways the system does not record?

It was built without accounting for these lives.

But it is sustained by them.

And until that contradiction is named,

there is no justice.

Only extraction with paperwork.

The next article traces where the money that should fund women’s lives actually goes—across borders, into tax havens, out of reach.

Note: This series is now being developed into a book, The Economic Ghost: Tax Is Not Math. It Is Power, which expands and deepens the analysis. For more, see [link].s the analysis. For more, see [link].

Comments